While the trajectory of the war in Iran remains highly uncertain – with the current ceasefire providing only temporary, and fragile, relief – the speed with which its economic impact has rippled around the globe is only too clear.

Given its high dependence on oil and gas imports, the UK appears especially exposed. Indeed, when responding to the evolving conflict last month by downgrading its global growth forecasts, the OECD suggested that the UK would be the most negatively affected of all G7 nations – a conclusion echoed this week by the IMF. The outlook continues to change on a daily basis, but what might any economic fallout in the UK mean for the nation’s charities?

Recent uneven recovery in living standards means significant numbers of people remain vulnerable to any renewed cost-of-living squeeze

Focusing first on the potential need for support that charities can expect to face, much will of course depend on how long the conflict persists. UK living standards have stagnated for much of the last two decades, but just how close to the edge are the nation’s households?

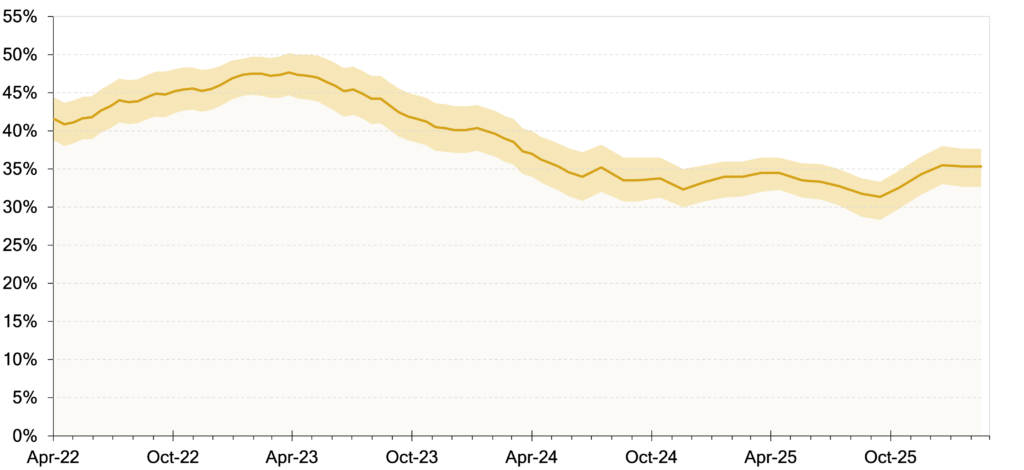

At one level, the domestic backdrop in place on the eve of the Iran conflict wasn’t quite as stark as it was at the height of the cost-of-living crisis. Figure 1 shows that the proportion of energy bill payers who say they are finding it “very” or “somewhat” difficult to afford their payments peaked at around 47% in early-2023 and then fell steadily to around 33% in the second half of 2024. The level has been broadly flat since then, albeit with some suggestion of a slight increase over the recent winter months. Following the Ofgem energy price cap cut from 1 April, we might expect the proportion to fall further still in the near-term, despite events in the Gulf.

Figure 1: One-in-three people continued to struggle with energy costs ahead of the Iran war

Proportion of adults who pay energy bills reporting finding it “very” or “somewhat” difficult affording these payments: Great Britain

Notes: Shaded area denotes lower and upper 95% confidence interval, which shows the range of uncertainty around the calculated estimate. As a general rule, if the confidence interval around one figure overlaps with the interval around another, we cannot say with certainty that there is more than a chance difference between the two figures. Solid line shows central estimate.

Source: Opinions and Lifestyle Survey from the Office for National Statistics

Nevertheless, typical energy bills will remain significantly higher than they were in 2021. And the cap will be reset – and likely rise considerably – in July. Moreover, the effects of the war on costs in other areas – especially at the petrol pump and in the supermarket – can be expected to land much more rapidly.

And of course, the Iran fallout does not exist in isolation. The cumulative effect of the tightly packed wave of economic shocks endured over the last two decades (the financial crisis, austerity, Brexit, pandemic, cost-of-living crisis) means that UK households are vulnerable to even a relatively short-lived period of disruption. Whatever the precise nature of the coming economic reverberations, we can expect significant numbers of people to be pushed back into difficulty.

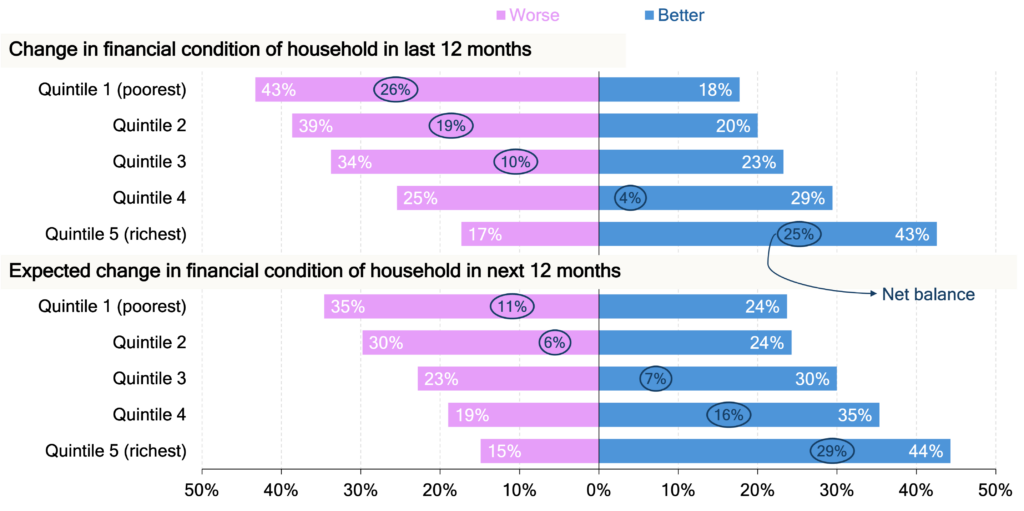

But it is not just the continued proximity to economic pressure for large parts of the population that should concern us: looking beyond the averages, it is apparent that the recent modest recovery in living standards has bypassed a significant minority, leaving them falling further down the financial cliff.

Figure 2 provides some sense of this imbalance. It shows that in the year to March 2025 – a period when average incomes grew as inflation fell and wages adjusted to catch up some of the ground lost in the prior two years – just 18% of households in the poorest fifth of the population said their own financial situation had improved. Instead, 43% said their finances had deteriorated. Conversely, in the richest fifth, 43% said their situation had got better and only 17% said it had worsened. And, while households across all parts of the distribution were more optimistic about the 12-months ahead, those at the bottom end of the scale continued to be more negative than positive on balance.

Figure 2: Two-in-five of the poorest households reported a deterioration in their financial positions in 2024-25, even as the wider picture on living standards improved

Reported and expected change in financial condition of the households in periods before and after March 2025, by equivalised gross household income quintile: UK

Notes: Survey conducted across 6,007 households between 25 February and 18 March 2025. Responses presented here relate to two separate questions: “How has the financial situation of your household changed over the last 12 months?” and “How do you expect the financial position of your household to change over the next 12 months?”. “Worse” covers those responding: “A lot worse” and “A little worse”; “Better” covers those responding: “A lot better” and “A little better”. Proportions are calculated after excluding the small number of respondents answering: “don’t know” and “prefer not to state”.

Source: PBE analysis of 2025 NMG Research Survey as published by the Bank of England in its ‘research datasets’.

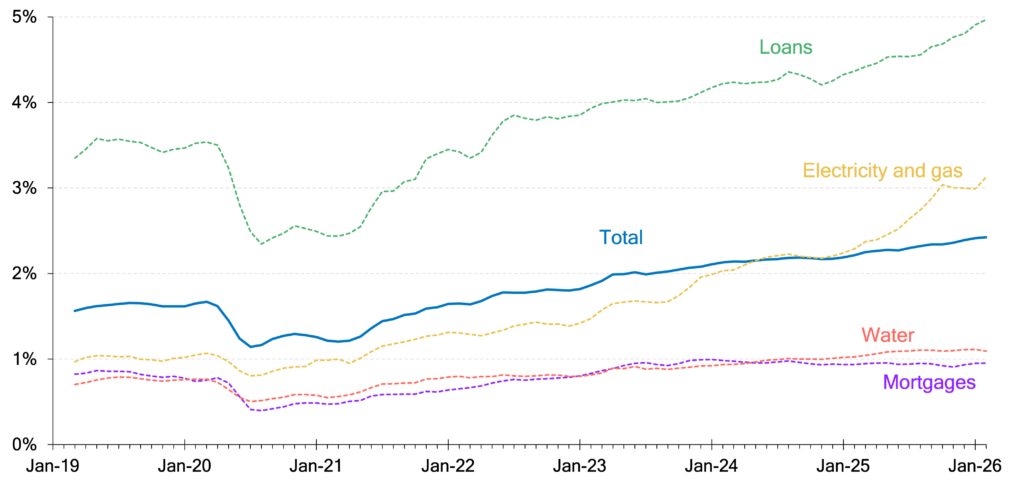

The strength of the continued economic challenge facing a sizeable minority is further displayed in Figure 3. It shows a doubling in the proportion of direct debt transactions ‘failing’ due to insufficient funds in customers’ bank accounts between February 2021 (1.2%) and February 2026 (2.4%). Failure rates vary across different categories of spending, with consumers clearly prioritising mortgage repayments over loans for example, but the relative pace of growth in failures (i.e. a doubling over the last five years) is consistent across all transaction types.

Figure 3: The proportion of direct debit payments that have failed due to insufficient funds has doubled over the last five years

Direct debit failure rate (total and selected sub-categories of expenditure), seasonally adjusted, three-month moving averages: UK

Notes: These data are made available by Pay.UK and Vocalink, respectively the operator of and infrastructure provider to the UK’s retail interbank payment systems. Vocalink process over 4 billion transactions annually, which include over 70% of household bills. These figures may not be representative of the whole UK Direct Debit failure rate. The ‘total’ failure rate includes but is not limited to the specified categories of spending.

Source: PBE analysis of ONS, Monthly Direct Debit failure rate and average transaction amount.

Relative to 2023 then, UK households appear to be under a financial strain that is perhaps narrower but deeper. The return of inflation to more ‘normal’ levels and a partial recovery in living standards appeared to signal the end of a near universally felt cost-of-living ‘crisis’. But for many the recovery remains fragile, and for a significant minority the economic backdrop has only become harder to navigate over time.

The skewed nature of the recent ‘recovery’ in living standards means demand for charity support remains elevated, leaving limited capacity for meeting a renewed surge in need

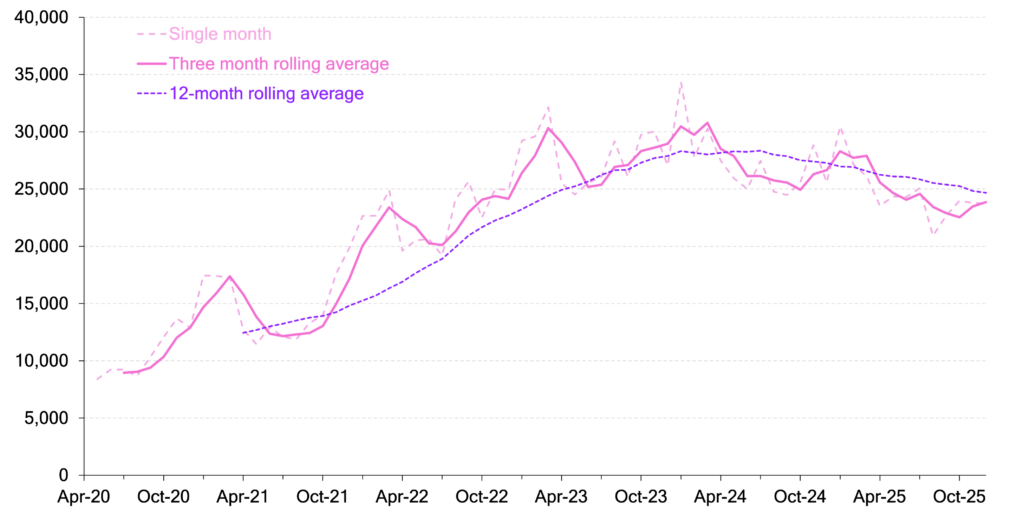

Figure 4 provides an indication of how this has played out for the UK’s charities. It tracks the number of people being referred to food banks and other sources of charitable support across local Citizens Advice offices and outreach centres each month. The trend shows just how rapidly the nation’s need increased over the course of the pandemic and its aftermath. While numbers have fallen a little over the last 18 months, demand remains significantly elevated. An average 25,000 people a month were referred in 2025, up from a monthly average of 10,500 in 2020.

Figure 4: The number of people referred to charitable support each month has more than doubled in recent years

Number of people helped by Citizens Advice charities with referrals to food banks or other charitable support: England & Wales

Notes: Data collected across 600 offices and 1,800 outreach locations across England & Wales. “Other charitable support” covers any emergency financial support or support in kind that people need to make ends meet.

Source: PBE analysis of Citizens Advice, Advice Issues

It’s a trend that is replicated in broader sector data, with 9% of people in England and Wales reporting that they or close family received food, financial or medical help from a charity in 2025, up from just 3% ahead of the first Covid lockdown.

These trends have been driven in large part by the remarkable run of crises faced over such a sustained period. But charities have also found themselves having to step in to plug gaps created by underinvestment in public services. On this front, some recent relief has been offered through budget increases in some areas. And the recent removal of the two-child benefit cap, along with Chancellor’s pledge to provide

energy bill support “for those who need it most”, will provide some further protection for lower income households. But it remains the case that spending increases have been both too narrowly focused and too small to fully reverse the damage done by a decade of austerity. The public sector doesn’t look well placed to share the burden of any sharp increase in need associated with events in Iran.

With prices of many supermarket staples already picking up – in a way that means the poorest tenth of households might be set to face a rate of inflation that is close to 1 percentage point higher than that experienced by the richest tenth – we can expect to see more people reaching out for help in the coming months. In many instances, that need will be increasingly complex and urgent given the depletion of households’ reserves of resilience that successive waves of economic shocks have prompted. Having continued to run hot even as the more universally felt cost-of-living crisis has faded from the headlines, the sector would appear to have limited capacity to meet that need.

Years of turmoil and a structural decline in support for the sector means many charities are likewise entering this new phase while already perilously close to the edge

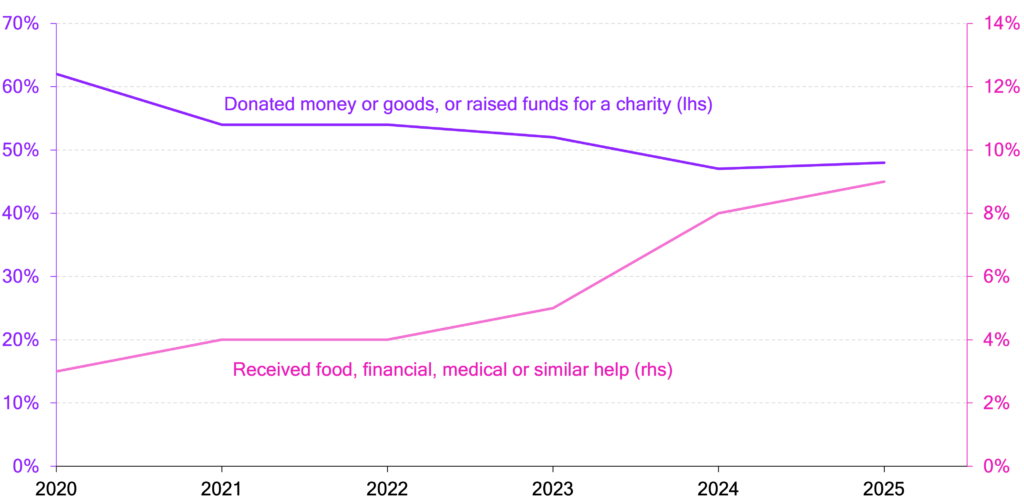

The sector’s capacity for taking on more in the coming months is further undermined by the fatigue and vulnerability being displayed by organisations that have been in crisis mode for a prolonged period. Especially when all of this comes against the backdrop of what appears to be a structural decline in giving by the public.

Figure 5 contrasts rising demand for charity help with a steady drop in public support. The proportion who say they or their close family supported a charity by either donating or raising money or by giving goods fell from 62% ahead of Covid to just 48% in 2025. Looking across a slightly longer timeframe, the Charities Aid Foundation believes that the UK has lost a remarkable 600,000 donors every year over the last decade, adding up to a reduction in the sector’s donor base of 6 million people. For some time that contraction has been compensated for by the increasing generosity of those who continue to give; but even that mitigation weakened in the latest data, leaving the total donated by the public shrinking year-on-year for the first time in five years.

Figure 5: The proportion of people supporting a charity has fallen steadily in recent years, even as the proportion leaning on charities for support has climbed

Proportion of people saying they or close family had supported a charity or used a charity in the last 12 months: England & Wales

Notes: “Have you or any of your close family had contact with a charity in the last year?” Base: All respondents: 2024 (4,599), 2025 (4,092). Latest wave of data collected in January 2025. All results are rounded to the nearest whole number.

Source: BMG, Public Trust in Charities 2025, Prepared for the Charity Commission for England and Wales by BMG Research, July 2025

The sector has been simultaneously hit by public sector budget cuts. Charities have long found themselves having to subsidise public funding, with 40% of organisations in receipt of such grants and contracts saying that they have “never” covered their true costs. But recent years of high inflation appear to have increased the size of the shortfall. Responding at the end of 2025, just 4% of charities in receipt of public funding said they had received uplifts in the past year that fully covered the true increase in the costs of delivering their services.

A renewed period of inflation and economic instability that puts both household and government finances even under greater strain clearly has the potential to accentuate both the trend away from public giving and the tightness of public sector funding. In simultaneously raising the costs (as cost-of-living pressures feed into higher wages) faced by charities themselves however, it will deliver a damaging double blow.

The irony of being asked to step up at precisely the same time that its own footing is under threat is one that the sector is well used to. But, coming as it does while organisations are still dealing with the consequences of prior crises, the challenge will this time be even harder to meet.

A majority of charities have consistently reported year-on-year deteriorations in their underlying financial positions in recent times. As a result, 41% of organisations currently report using reserves to meet day-to-day operating costs, with a further 12% saying they have no reserves at all. Meanwhile, both charity closures and mergers have increased in recent years. In terms of the latter, not only were numbers up in the latest figures (49% year-on-year), but so too was the proportion of charities recording a financial deficit ahead of their merger. The implication is that the trend is being driven by financial imperatives rather than strategic choices.

Once more then, the charity sector must brace itself for the increase in need that always accompanies economic turmoil. But much like the nation’s households, organisations across the charity sector enter this period carrying the fatigue and the scars of previous battles.

The sector always displays courage under fire, but it needs to win the peace too

Difficult though the backdrop is, charities must not succumb to fatalism. We do not yet know how the conflict will unfold, or how sharply its economic effects will be felt at home. But the sector has repeatedly shown its ability to adapt and respond, even as pressure on its resources grow. At the same time, it would be a mistake to assume that charities can simply stretch further once again. The organisations people rely on are entering this period already weakened, and their resilience should not be taken for granted. Supporting civil society through the months ahead will require concerted action across the public, private and social sectors.

Some of the pressures charities face are cyclical and may ease as economic conditions stabilise. Others are more structural, including longstanding weaknesses in funding models and a declining culture of everyday giving. Successive shocks have left little room to address those deeper issues, and the risk now is that renewed disruption further crowds out the space needed for reform.

That points to a dual task. In the near term, those with resources should be prepared to step up as need increases. In parallel, longer-term approaches must be strengthened: providing greater predictability for grantees, smoothing transitions in funding, and rebuilding a charitable system that is more resilient to shocks.

Government, funders and business all have a role to play alongside charities themselves –from reinvigorating incentives to give, to ensuring public funding reflects the true cost of delivery, to supporting collaboration and mergers where they strengthen services. None of this is easy, particularly in a volatile environment. But treating each crisis as an isolated episode, rather than as part of a sustained period of strain, risks further attrition across a sector that remains central to the UK’s social and economic wellbeing.

Whatever course the conflict in the Middle East takes, maintaining a clear and sustained focus on the health of civil society will be essential – not only in times of acute challenge, but in the calmer periods that hopefully follow.